As incomes of today’s young people rise, they will become the main customers for banks in emerging markets. But the gap between what they want from banks and what’s on offer is often very different.

Source: Shutterstock

As incomes of today’s young people rise, they will become the main customers for banks in emerging markets. But the gap between what they want from banks and what’s on offer is often very different. Millennials value convenience and mobility and expect a digital solution for everything—and currently, they are dissatisfied with standard banking services.

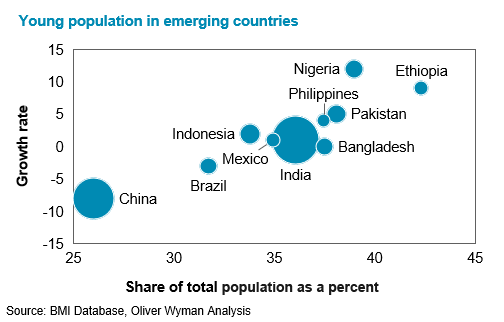

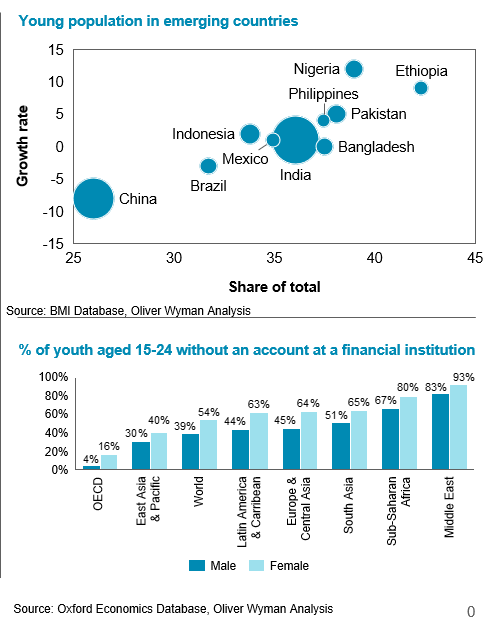

That’s a danger to banks because it gives millennial-savvy businesses an opportunity to scoop them up as customers. Many emerging market banks have neglected younger customers so far. Instead, they cater to older customers who have more money and, therefore, look like a better business prospect. Often, banking services customers stick with a provider for many years, so retail banks need to start offering what the younger customers—ages 10 to 29—demand, as they represent between 30 and 40 percent of the population in emerging markets. Banks should start investing now, as it will take a few years to build up the necessary products and develop credibility.

To become more attractive to young consumers, banks should work in three broad areas: digital products and services, communication and customer relations.

Create Digital Products and Services for Young Customers

Young people have grown accustomed to digital and mobile interaction, as it becomes the primary channel for use and payment in industries such as entertainment and retail. To address this reality, banks need to reach out to millennials through a digital channel that gives them access to all their banking services.

The best-known mobile financial product is Chinese e-wallet WeChat Pay. It emerged from the messaging app WeChat and has since become a major part of Chinese consumers’ daily lives. It is used for payments in taxis, supermarkets and hospitals, for example. On the Quick Pay page, vendors can scan a QR Code shown by customers on their smartphones to complete transactions quickly. Customers can scan products’ QR codes to see details and then make a purchase. WeChat also carries out cross-border payments in yuan in at least 10 other currencies.

Similarly, in Brazil, Banco Original appeals to millennials by basing its business on five pillars. Its services are, the bank says, innovative, accessible, simple, secure and transparent. Banco Original gained 1,000 clients per day in the first quarter after its 2016 launch. In 2017, it grew at 134 percent and reached a market share of 11 percent. Mobile and electronic money are likely to become important in other emerging markets, too. In the Economic Community of West African States, for instance, they are forecast to rise to 45 percent of retail payments in 2021 from 20 percent in 2016.

Attract and Communicate with Customers

Young people prefer to interact digitally rather than physically or over the phone. Only 49 percent of survey respondents in Generation Y (23 to 37 years old) preferred to communicate with banks on the phone, according to Forrester Research. That fell to 38 percent for Generation Z (16 to 22 years old). Moreover, young clients are looking at social media as a source of information.

To respond to these preferences, the 811 digital bank account—dubbed a “new-age bank account” and launched by Kotak Mahindra, India’s fourth-largest private sector bank—allows customers to sign up via an app with just a national identity number.

Even if banks do not interact physically with their customers, they can understand and engage customers through the growing number of touchpoints and increasing amount of data available from social media and via smartphone apps. Analysis of these data can track key trends and conversation topics, as well as seasonal patterns and spikes in conversation volumes at certain times. Detailed customer profiling data—such as age, sex, location, occupation and status—can then provide information for segmentation to help enhance customer experience, optimize banks’ marketing strategies and reduce risks by monitoring complaints and reactions to change.

Millennials tend to judge banks in terms of image and values, making branding especially important for them. They are attracted to brands that are cool, fun and social. They also value brands that have a positive buzz and are valued by their peers. Since traditional banks do not convey those values, they should create a separate sub-brand to attract the younger segment of customers.

In Singapore, for instance, OCBC has developed FRANK. Its advertising uses minimal financial jargon, emphasizes special pricing for younger clients, and shows bright, fashionable young people enjoying themselves at work and at home. The brand suggests honesty, trust and progressiveness.

Its name comes from the adjective for clear, simple, honest expression and comes with a tagline: “FRANK—saying it as it is.” Four years after its launch, FRANK had captured 70 percent of Singapore’s young working adult segment.

To access a wider base of clients, banks should consider partnerships as a way to reach still-unbanked people. Many telecommunications companies have accumulated a base of customers; other potential partners include operators of mobile apps, schools and malls.

Foster Loyalty through Youth-Friendly Business Terms

At first glance, the young are a relatively unappealing market segment due to their limited income. However, as they grow older, they become wealthier and require financing for life projects, such as home mortgages and education loans. Since customers often stay with their first bank, it is important to forge relationships with young customers.

In mature markets, banks focus strongly on the student market to capture a share of the next generation of customers before their rivals. In emerging markets, they try to help young people improve their lives at important moments, so as to build long-term relationships and customer fidelity. HDFC Bank in India offers targeted products and services that support younger customers—a children’s account to encourage financial literacy in younger children, for example, and products to fund education as they grow older.

Millennials have limited financial means, and they dislike regular fees. In Brazil, Banco Inter does not charge a monthly fee or fees for a digital account, card subscription or interbank transfers. Its promotional materials explain that it can do this thanks to the low cost of an automated, all-digital process, plus revenue streams from credit cards and loans.

When they do have to pay fees, the young demand clear and transparent pricing, including a simple structure and payment schedules. Fair, transparent pricing can foster trust, which helps retain customers. Moreover, customers who feel they are getting a good deal will refer the bank to other potential customers.

Though millennials want to be treated as valued customers and want their loyalty to be rewarded, they are the least loyal of all customer segments and tend to switch banks very easily. In Asia, 33 percent of millennials would be willing to switch banks in the next 90 days, and 71 percent don’t see their interactions with banks as a relationship, but as a transaction. Special rewards programs and financial literacy programs can help to engage young customers, foster loyalty and build a sustainable client base, producing steady revenues. Rewards can include personalized offers based on spending patterns and profiles, product bundles, goal-based products and incentives for referral. In Australia, for instance, CommBank has developed a schools banking program that teaches young clients how to save through a reward and gift system.

Today’s Young—Tomorrow’s Revenues

In emerging—as other—markets, today’s young people are tomorrow’s lucrative client base for banks. So far, however, many banks have not paid sufficient attention to this age group or taken action to attract them. The exceptions show that there are ways to do this.

But banks need to act fast. If they don’t, others will. Some of these rivals will be competitors in the banking sector, but others will be nonbanks that are increasingly providing the essential services—such as savings, loans and payments—that have traditionally been carried out by banks.

{kind=link}