Blockchain technology has the potential to revamp trade around the world and restore trust in the global shipping business.

Photo: David McNew/Getty Images

International trade is under pressure. Fears fueled by the global refugee situation and terrorist threats have led to tighter border controls—and these come at a cost. Every inspection of goods, every stop along the supply chain, eats up time and drives up prices. It harms businesses and consumers alike. Those involved in international trade—whether they are manufacturers, trading houses, transportation companies or banks—are seeking ways to ease the situation and cut time and costs.

Blockchain technology can help. The cloud-based ledger ensures that records can’t be duplicated, manipulated or faked, and increased visibility in parts of the supply chain promotes an unprecedented level of trust. It means governments can better protect citizens, while business partners can be certain trading documents are real. Consumers can check the quality and provenance of products, and banks can reduce processing time. And it’s all paperless.

Thanks to blockchain, all kinds of legal, financial and product-related information can be made available. This allows even the least trusting parties to comfortably conduct business. With further investment and experimentation, blockchain could potentially hide confidential information—pricing information, for example—to protect the interests of trading parties.

Does it work in the real world? Barclays reported the first blockchain-based trade-finance deal in September 2016. The transaction guaranteed the trade of almost $100,000 worth of cheese and butter between Irish agricultural food co-operative Ornua and the Seychelles Trading Company. The process—from issuing to approval of the letter of credit, which usually takes between seven and 10 days—could be reduced to less than four hours.

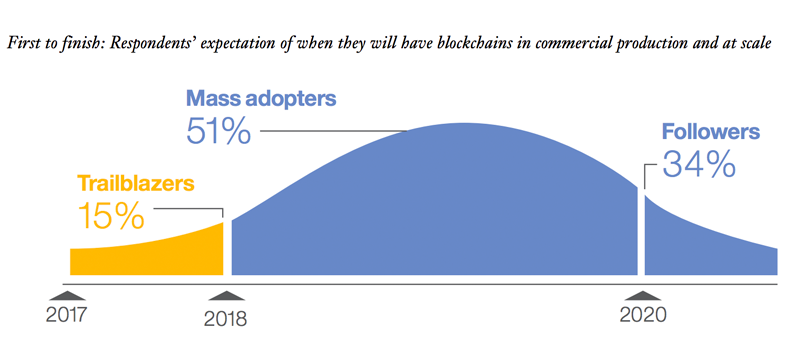

Source: IBM, “Leading the Pack in Blockchain Banking: Trailblazers Set the Pace”

Other banks are also exploring ways blockchain technology can improve processes along the supply chain. In August 2016, banking consortium R3 reported that 15 of its members had joined a trade finance trial to test its distributed ledger protocol, named Corda. Also in August, Bank of America, HSBC and the Infocomm Development Authority of Singapore revealed that they had built a blockchain application to improve the letter of credit (LC) transaction process between banks, exporters and importers.

It’s not only banks: Maersk, the world’s largest container-shipping line, has been participating in a proof-of-concept initiative, using blockchain expertise from the IT University of Copenhagen to digitize the ships’ cargo inventories. These so-called “bills of lading” require an enormous amount of paper. A shipment of roses from Kenya to Rotterdam, for example, can result in a pile of paper nearly 10 inches high. And the cost of handling it can be higher than the cost of transporting the containers. Maersk’s aim is to optimize the flow of information while raising visibility along the supply chain.

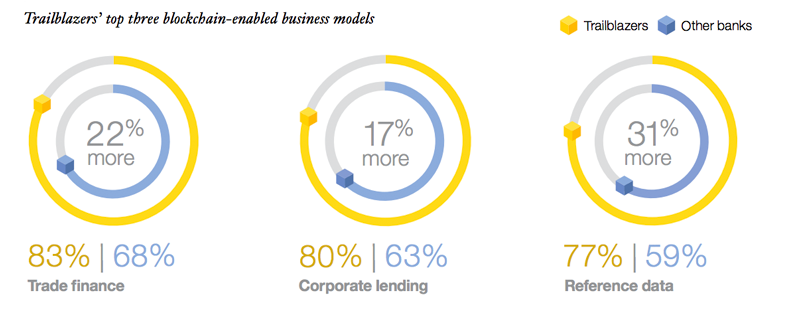

Source: IBM, “Leading the Pack in Blockchain Banking: Trailblazers Set the Pace”

Often when making a purchase, buyers don’t know where the goods they ordered are coming from, or even whether they have been shipped at all. With blockchain, consumers can be informed of every step in the process. Combined with the Internet of Things, this could also extend to the care with which a product is transported. Swiss startup Modum.io, for example, uses blockchain as a way of assuring recipients that pharmaceuticals have remained within an acceptable temperature range while in transit.

Trust and Transparency

Citizens are worried that reduced barriers at the borders, as well as trade agreements, increase the risk of terrorism and illicit trade. Blockchain technology can, in fact, provide the backbone of a system of authorized trusted participants, bringing everything into the light, whether it’s a product, the party selling it or the path it takes to reach the buyer. Consumers and watchdogs, public and private, can trace every item moved through the authorized blockchain-backed channel and validate or reject both product and party. Customs clearance, too, can be optimized using blockchain. Parties that are part of the group can act quickly and efficiently while others may face scrutiny.

Immutable records on every aspect of a transaction—from the source of the raw material to where and how the products were manufactured, to their distribution, maintenance, repair, recall and recycling histories—are the new basis of trust. Information about ownership, provenance, authenticity and price are all held in the blockchain.

Digital product memories connected to smart devices along the supply chain will provide secure proof of everything from manufacturing processes to quality controls. This will reduce the cost of compliance, i.e., the adherence to laws and regulations. Furthermore, this will open doors for replacing current product labeling practices to protect consumers and accelerate customs-clearance processes. Customers and consumer-protection organizations, as well as customs authorities, will have all the information they need to decide whether to buy or not to buy, to let goods through the border or to block them.

Blockchain has the potential to become the new gold standard of business and trade. But first, all nations need to accept the new technology. There are technical hurdles to overcome. First, blockchain protocol(s) used to secure the ledger of global trade and manufacturers must be trusted by all of its users and be effectively un-hackable. Technical capabilities to handle very large transaction volumes will also need to be enhanced, and the cost of maintaining the protocol may need to be lowered. Ordinary companies and individuals will need to be onboarded to the machine-to-machine (M2M) economy. The liability model of trade conducted on the blockchain will need to be reviewed as the appropriate treatment of liability may differ from current models.

Blockchain can help to reinforce trust in today’s complex and globalized world—giving citizens and governments fresh confidence in the global exchange of goods.

This piece first appeared on the World Economic Forum’s Agenda Blog.