A general view of the central business district in Beijing, China.

Photo: Lintao Zhang/Getty Images

China’s fintech market has grown rapidly in recent times, but the potential for the sector’s growth in China remains massive. Against that backdrop, the ability to develop and apply cutting-edge technology will be increasingly important for tomorrow’s fintech leaders in China if they are to make the most of this phenomenon.

While different types of players will attempt to penetrate the market, we don’t believe there is a one-size-fits-all formula for success, but rather that certain factors can increase the likelihood of success.

Key Success Factors

We see five major key success factors for the future China fintech market:

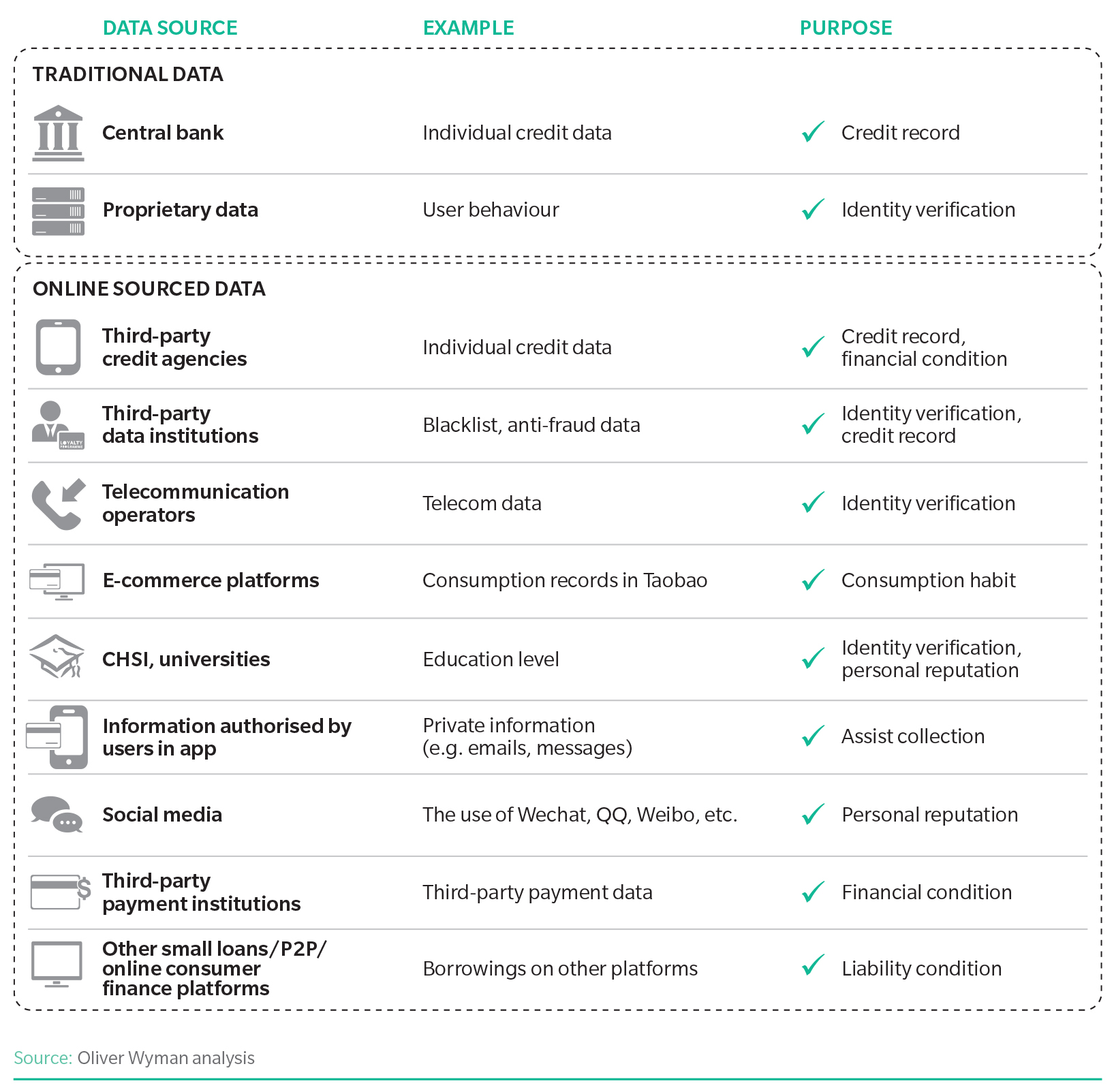

1. Data abundance and application: Business models in financial services will be increasingly data-driven, and data will be at the core of the value chain. Therefore, innovation and impact in future fintech will be greatly helped by access to or ownership of large amounts of proprietary data, as well as the ability to derive insights from the data (Exhibit 1).

2. Large customer base: A large customer base will complement data capabilities, completing a virtuous cycle of mutual benefits for fintech players and their customers. First, fintech companies can apply data-driven insights to monetize their large customer bases, deriving direct economic value from the data. A large customer base, in turn, allows for faster accumulation of valuable data that can be analyzed to further improve products and services for customers, risk management and dynamic pricing.

Exhibit 1: Available data sources for credit-risk management

3. Availability of proprietary and comprehensive products: Chinese consumers will increasingly seek unique, proprietary products. Fintech players will need to develop adequate scale and obtain necessary licenses so that they can offer a comprehensive suite of products to satisfy their customers’ needs and differentiate themselves from peers.

4. Strong knowledge of financial services and risk management: A strong combined core of financial services expertise and risk management capabilities remains a prerequisite for success, allowing for more efficient identification of useful data and building of effective risk models.

5. “Fin plus tech” organization and culture: Constant innovation will be crucial in the future of fintech, and the right operating model and culture will be integral to success. This implies a lean, flat organizational structure with product-driven teams comprising both financial and technology talents in order to shorten product development cycles through hypothesis-driven experimentation and maximize returns by tailoring products for customers.

Implications for Fintech Market Participants

During the explosive growth of fintech in China in recent years, we have witnessed the establishment of four major types of players, with each type of player possessing its own strengths and weaknesses. Such dynamics result in rather different strategic foci for each type of player.

All-around Fintech Players should maintain their advantages by cementing their pioneering roles in the fintech space through technology-enabled innovation. First, they should continue to build their customer base and drive innovation using insights derived from their massive data pools. Second, using this abundance of data and their insight-generating capabilities, they should identify opportunities for needs-based cross-selling of financial services products. Third, given the recent regulatory trends, they should proactively apply for necessary licenses to sustain their business models.

Niche Fintech Players should expand and perhaps transform their business models. The first and most intuitive way is to grow organically beyond a niche. Qudian, for example, has expanded beyond its legacy focus on university borrowers to develop an e-commerce ecosystem driven by a consumer finance model. At the same time, we anticipate mergers between some niche players to consolidate their strengths and resources. Some players are actively considering expansion outside China in order to replicate their success in markets with similar needs, such as Southeast Asia. Since banks and all-around fintech players are dominant in their customer base, niche players could export their technological know-how to partner with traditional financial institutions.

Traditional Financial Institutions should build data capabilities under flexible organizational setups. First and foremost, they need to create leaner structures and culture with operating models that are more suitable for fintech. This could also be done by setting up separate business units with more-independent authority and decision-making processes. It is important for traditional financial institutions to then invest in data processing capabilities and infrastructure to effectively monetize the traditionally offline customer base by leveraging on innovative data sources.

Players from Non-Financial Industries should carefully consider whether and how to best leverage their strengths and large customer bases to expand laterally into the fintech space. For example, logistics providers such as S.F. Express possess proprietary information on massive daily inventory flows, which is then incorporated into a risk-assessment methodology and used to power their supply chain financing and consumer lending ventures.

Implications for Fintech Investors

Capital investment in China fintech is hotter than ever. However, as the development dynamics of the industry are bound to change in the future, we believe that China fintech investors should follow the four key rules below.

Avoid overvaluing regulatory arbitrage. The historically open regulatory environment was one of the major growth drivers for a lot of fintech players. But tightening regulations are bringing the age of arbitrage to an end and will likely have a negative impact on fintech expansion. So, investors should identify targets’ underlying growth drivers and avoid overestimating future value driven by regulatory arbitrage.

Explore the broader landscape. The integration of fintech into the regulatory framework has, to a certain degree, leveled the playing field for traditional financial institutions such as banks and securities firms. The recent strategic partnerships with fintech players by China Minsheng Bank and the introduction of online lending products by ICBC are just a few signs that fintech investors should start looking beyond fintech startups.

Assess the potential downside. Despite not bearing credit risks in legal terms, fintech platforms could face reputational losses, regulatory actions, and even liquidations due to potentially problematic products. This has been illustrated by the cases of Ezubao and Zhao Cai Bao. Although the number of such products will likely diminish under the tightening regulations, investors ought to be aware of downside scenarios and diligently assess their potential impact.

Capture value from technology and the surrounding infrastructure. As technology-enabled disruption is the main trajectory for China fintech, investors should look beyond the actual innovative solutions and products. There is also value in the infrastructure enablers behind such products, such as large user bases for trials, access to proprietary data for analysis, and agile fin plus tech governance structures.

While current leaders might be able to build on their strengths and expand on all fronts, the chaser pack could still find major places for themselves by applying differentiated technology in spaces where it is needed. Strategic planning, significant and rightly directed investment and prompt action are required for tomorrow’s Chinese fintech leaders. The fintech landscape in China is evolving fast—only those who weigh it right will be able to hit gold.

The first part of this piece was published last week, focusing on the fintech market’s growth in China and the financial and technological drivers for growth.