People work at dusk on various floors of an office development in London, England. In light of new digital transformations, directors must recognize these technology trends and understand how they might threaten existing business models or drive business model innovation.

Photo: Oli Scarff/Getty Images

Automated retail kiosks, robotic processes, autonomous vehicles and digital payments are all innovations shaping how the lives of consumers and workers are being streamlined. The economic value generated from these new digital solutions and business models combined with the speed of their adoption is staggering. In fact, the World Economic Forum estimates that the combined value of digitization in every industry could generate upward of $100 trillion over the next six years.

Given the near-term disruptive potential of new business models that are enabled by emerging technologies, many boards are actively reassessing their oversight role in governing digital transformation initiatives. As stewards of long-term value creation, boards will need to strengthen their oversight of digital transformation and emerging technologies.

What Does the Road Ahead Look Like?

Though directors are realizing that the current state of technology oversight at their companies may be insufficient to fulfill their fiduciary duties, they may also not know what a road forward should look like. Several challenges stand in the way of board readiness in this area, including:

- A lack of clarity on what digital transformation entails.

- Metrics that are inadequate for acceptable oversight.

- Ingrained habits about board composition that block the necessary talent from stepping onto the board.

- A prevailing, largely protective oversight bias driven by recent attention to cyber- and data privacy risk.

How can directors enhance their oversight approach and confront these challenges?

A new report, Governing Digital Transformation and Emerging Technologies, developed jointly between NACD and Marsh McLennan, offers five flexible and practical governance principles for oversight of digital transformation and emerging technologies.

1. Approach emerging technology discussions as a strategic imperative — not just an operational issue.

All members of the board should prioritize understanding how new technologies could solve specific business operations or customer experience problems. Additionally, board members and their management teams should have a shared, well-defined vision of the business goals required for going digital. Is the objective to increase efficiency, accelerate growth or develop new partnerships? Defining objectives will focus allocation of resources and identify time horizons to success. Finally, board members can evaluate whether management is thoughtfully building the necessary conditions to drive change in the long term and help management assess how core businesses and capabilities will be impacted.

2. Develop specific goals that lead to continuous learning about technology.

Directors cannot appropriately oversee what they don’t understand. When they don’t feel prepared to engage management on emerging technologies, they are not fulfilling their fiduciary duties. Continuing education will be critical to bridging this gap. Boards should adopt a mindset of ongoing learning and development that supports effective oversight of emerging technologies. These learning objectives should support the board’s oversight of the exploitation and risk mitigation of adopting new technologies. Goals should be developed by assessing collective and individual director knowledge gaps and skills and should inform future recruitment needs.

3. Realign board structure and composition to reflect the growing significance of technology risks.

Given the pace of change, the stakes for having individuals with technology experience in the boardroom are high. Boards would be well-served by assessing whether their current composition and structure will continue to be fit-for-purpose in delivering effective oversight. Some boards are addressing this by recruiting directors with digital expertise, though this practice remains uncommon; the need for the recruitment of a digital director may not apply equally to all boards. But for those boards that deem the expertise necessary to fulfill the board’s fiduciary duties, the recruits should have business acumen, a commercial track record and governance experience. Notably, the addition of a digital director doesn’t absolve the rest of the board of their responsibility to oversee technology-related initiatives.

Boards are also exploring changes to committee structure. These committees can focus on risks, investments, the renewal of technology, business continuity, technology talent and controls. When determining whether to establish a technology or innovation committee, directors should avoid making hasty or uninformed decisions, as doing so can result in vague and ineffective mandates. Instead, boards should carefully weigh the merits and risks of establishing a dedicated, board-level committee for oversight of this issue.

4. Demand frequent and forward-looking reporting on technology-related initiatives.

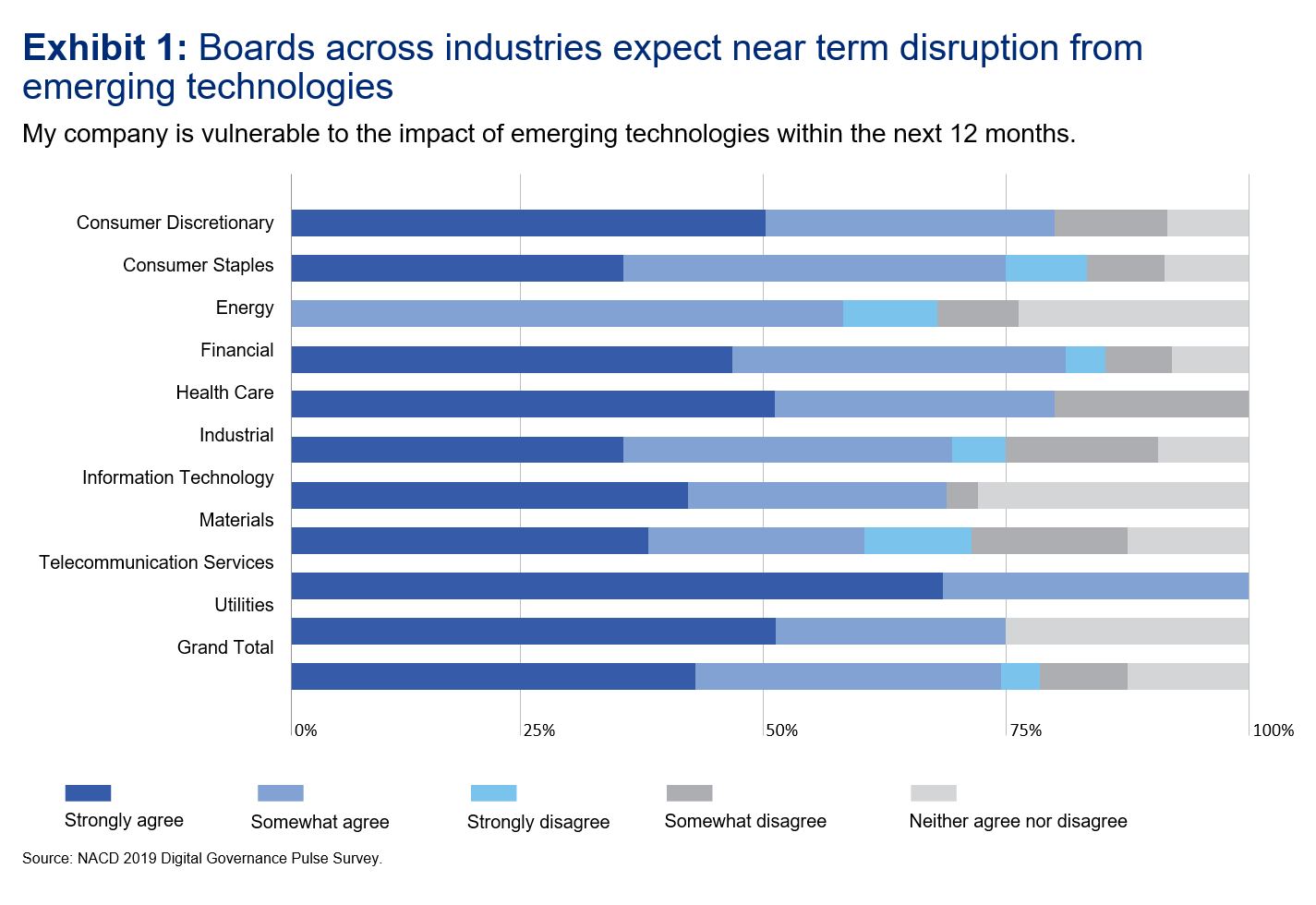

Many directors struggle to assess how technology makes a meaningful impact on business performance. According to the report, 65% of directors found metrics on the effect of emerging technologies to be inadequate and a critical barrier to delivering effective oversight of technology. As boards request related metrics from their management teams, they should require forward-looking visibility into technological disruptors and how they will affect the company’s strategy.

Directors should establish clear reporting guidelines to ensure that they receive transparent, actionable and succinct information for their oversight. Finally, boards and management teams should focus on metrics that are clearly tied back to the business objectives. The metrics should include targets or indicators that signal whether a long-term effort is on track or stalling.

5. Periodically assess the organization’s leadership, talent and culture readiness for technological change.

A company’s people — employees, vendors and contractors — are at the core of its business. As such, there can be no digital transformation without workforce transformation. As companies set about transforming their business models and strategies, corporate leaders need to prioritize the recruitment and retention of a workforce that is properly positioned to support business goals. Leading companies need management teams that have the expertise to carry forward a technology-enabled vision. As they recruit and evaluate the CEO and executive team for technology leadership, directors can focus on experience in digital strategy, a reliable record of delivery, demonstrated ability to drive organizational change and confidence to face challenges head-on.

Innovation cannot be achieved by members of management alone. Directors should also assess the strength of corporate culture in every corner of the business, ensuring that change, innovation and experimentation are characteristics embraced across ranks. Organizations can’t encourage risk-taking and simultaneously punish commercial failures. Directors should ask management to develop an integrated human capital strategy that identifies the necessary elements to deliver on the company’s future strategy and incorporates retraining, a plan for talent retention and a skills inventory of the current workforce.

Boards recognize the need to actively reassess their oversight responsibilities in governing digital transformation initiatives. To succeed, directors don’t need to be experts on every technology trend, but they will need to understand how new technologies can threaten existing business models or drive business model innovation. These guidelines offer an actionable framework for directors seeking to ensure their companies reap the commercial benefits of digital transformation and emerging technologies.

This piece was first published on the NACD BoardTalk blog.