A bank employee counts Indonesian currency in Jakarta. Asian banks today account for 40 percent of total global assets, compared to 27 percent in 2009.

Photo: Adek Berry/AFP/Getty Images

The Asian banking sector can claim an outstanding record from past years; however, a new report casts doubt on whether the sector’s outstanding performance can be maintained with any certainty in the coming years.

The sector has expanded its size, measured in total assets, by about 70 percent since the global financial crisis. Asian banks today account for 40 percent of total global assets, compared to 27 percent in 2009, partly as a result of North America and Europe reducing their risk-weighted assets. In addition, Asian banking has achieved this top-line growth while maintaining its return on equity (ROE) above 10 percent—a clear premium compared to other regions.

The report outlines a much less predictable future for the Asian banking sector and creates a sense of urgency to act based on the following:

- Macroeconomic growth is slowing down

- Past growth has pushed debt/GDP ratios into critical territory

- Non-performing loans (NPLs) are rising

- Global trade and capital flows are being challenged in light of a strengthening U.S. dollar and looming protectionism

- Digital disruption is challenging traditional business and operating models

As a result, metrics, such as net interest margin (NIM), are coming under pressure, and confidence in Asian banking has been dented. Compound annual growth rates (CAGR) in assets have slipped to around 5-7 percent compared to nearly 10 percent in the recent past. Banks will need to work with even lower baseline growth scenarios in the next few years—which will cause declines in ROE.

Navigating the New Environment

Asian banks that want to successfully steer through this new environment should take action across five dimensions.

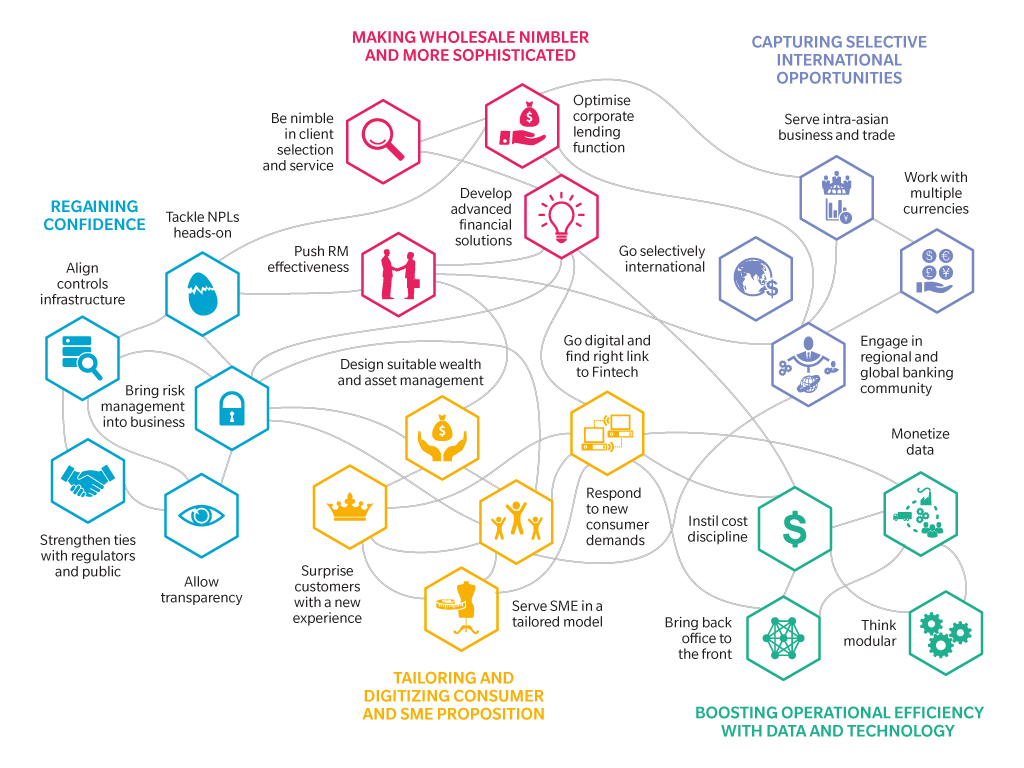

Regaining confidence. Many Asian banks suffer from concerns about the quality and stability of their books, primarily triggered by high corporate and private leverage, rising NPL in several Asian markets and potential asset bubbles. To regain confidence, Asian banking should proactively provide greater transparency about the quality of its balance sheets; tackle high leverage and NPL head-on; improve effectiveness and efficiency in its controls infrastructure in risk, compliance and audit; move risk management closer to the front office; and strengthen positive ties with regulators and the public around risk culture and ethics.

Becoming more nimble and sophisticated in wholesale. Corporate and institutional banking is the backbone of Asian banking, and historically it has been driven by lending to large companies. Pressure on economics in plain vanilla lending and client need for more sophisticated services require a transformation of the traditional wholesale banking model, including becoming more nimble and differentiated in corporate client selection (including an ecosystem-led approach) and service model; advancing relationship management effectiveness; and increased efficiency through digitization, professionalizing underwriting, and shifting to capital-markets-based financing.

Tailoring and digitizing consumer- and small- and medium-enterprise (SME) propositions. Retail banking is a main growth area in Asia, partly driven by financial deepening (in emerging Asian markets, for example) or driven by high wealth levels and evolving demands of a changing society (in more mature Asian markets, for example). To capitalize on these opportunities, responses need to be nimble and tailored for individual markets and segments. Four broad themes are quite consistent across the region: responding to fast-evolving new consumer demands, better serving the SME space, developing a next generation wealth and asset management offering, and surprising customers with a more emotional experience and going digital along all these topics, including finding the most effective link with fintech.

Capturing selective international opportunities. Asian banks face a conundrum when designing their international strategies: The global political landscape is changing. Global trade and capital flows are being challenged, but Asian commercial integration is continuing, fostered by bold initiatives like the Belt and Road Initiative. Foreign exchange markets have become volatile and the growth of renminbi (RMB) as a currency in trade has slowed down a bit. Some global banks are retrenching while many Asian banks would have the scale to fill the opening gap, but they might be hesitant because of mixed experiences in the past. At this point, Asian banks need to focus on the longer-term, and we suggest they capture selective international opportunities along four areas: serving intra-Asian trade and business connectivity, going selectively international where others retrench with the right mix of buying/building/partnering, preparing to work with multiple currencies (especially the RMB), and networking in the regional and global banking community. All of those efforts should serve the longer-term goal for Asian banks to capture opportunities on an international scale when they arise.

Tackling operational efficiency, data and technology. Most Asian banks have benefitted from top-line growth at stable and high NIMs. Therefore, operational efficiency, best use of technology along the value chain and cost discipline all have been less of a priority for many Asian banks when compared to their European or North American peers. With a potentially more volatile outlook, Asian banks need to improve their operational efficiency and their use of technology along the value chain, mainly touching four topics: developing a more modular and agile operating model that can serve more complex business needs, instilling cost discipline, using technology for efficiency along the value chain, and advancing the effective use of data and analytics.

Asian Banking Agenda 2017

Source: Oliver Wyman

Sifting the Best from the Rest

Banks that deliver well across the five dimensions illustrated above will perform well within their regions. For the sector as a whole, the following important initiatives will decide between winners and losers within certain geographies and also across the whole Asian market:

- Taking advantage of financial deepening and successfully providing digital value propositions in the retail and SME segments

- Improving capital efficiency through risk management

- Transforming traditional lending-based wholesale banking to become more innovative

- Becoming more nimble in underwriting/client coverage

- Heightening focus on operational efficiency

Delivering on all these areas requires alignment across all bank segments and geographies. Asian banks that manage this complex environment well will do better than the rest and will be set to further expand their businesses toward the forefront of global banking.