In Sweden, some firms are making on-the-job exercise compulsory for their employees. Western consumers are taking a more active approach to their own health.

Photo: Jonathan Nackstrand/AFP/Getty Images

The rise of consumerism in health care has the potential to transform the entire sector. Health care is evolving from a sick-care market—treating people who are already sick—to a consumer-driven health market, where consumers take control of their health and wellness decisions.

Three main factors are driving this shift. Firstly, the costs of being sick are escalating, creating a crisis for consumers who have not yet switched to more active management of their own health. Secondly, new technologies are empowering consumers; multiple solutions such as wearables and virtual care such as video calls with doctors are becoming more mainstream, allowing consumers to find alternatives to the traditional health care approach. Last but not least, governments and payers are encouraging this change, because it reduces costs through preventive care and the cheaper management of chronic conditions.

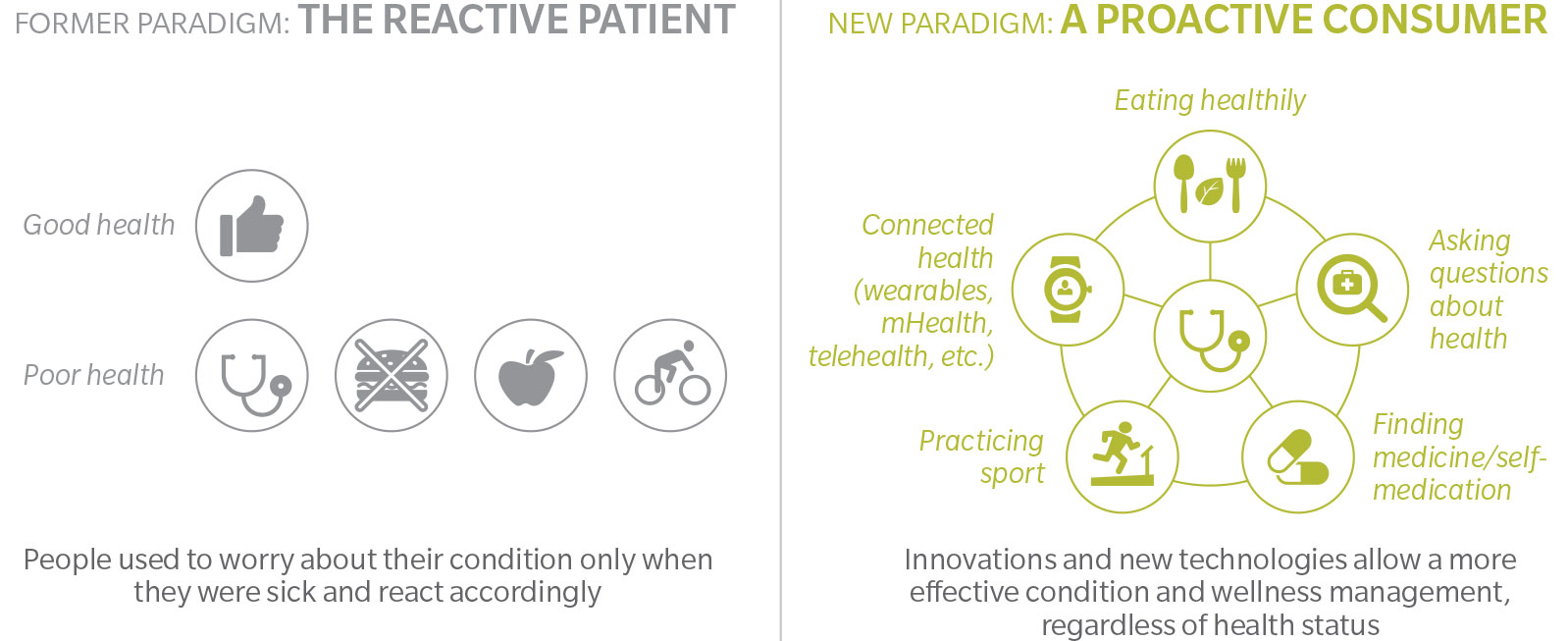

We are calling this new paradigm, “Health 2.0.” (See Exhibit 1).

Exhibit 1: Health 2.0 new paradigm: the consumer-driven health market

Source: Oliver Wyman analysis

Direct to the Consumer

The rise of consumerism in health care offers a new outsized opportunity in direct-to-consumer categories. January’s announcement from Amazon, JPMorgan, and Berkshire Hathaway clearly heightens this pressure. This groundbreaking news confirms that health and wellness are major aspects of consumerism’s future direction. As potentially industry-shaking partnerships such as this come to fruition, the question is: “Who’s in the best position to stake a claim in this about-to-explode market?”

Recent innovations include foods that offer health benefits, for example, better digestion and healthier skin, and wearables that track fitness activity and sleep patterns. A future market of services and offerings will allow consumers to take charge of managing their vital signs, behavioral health, and wellness.

This consumer health market is predicted to double in size by 2020. This steep growth is, understandably, gaining the attention of different types of organizations—from traditional players (pharmaceutical companies, hospitals, doctors) to retailers and consumer packaged goods companies (CPGs).

How Will Traditional Providers React?

Traditional incumbents may struggle to respond to this opportunity. They generally haven’t managed people’s health care over multiple years because their incentives and profit model do not align with this approach.

But some forward-thinking payer and provider entities are successfully engaging consumers outside health care’s usual boundaries via nontraditional offerings. In diabetes or heart disease, for example, some organizations realize successful outcomes can’t be achieved only by treating the problem reactively, that is, once the symptoms have appeared. They recognize the opportunities to engage consumers through everyday areas of contact such as nutrition, exercise, and social support by proactively managing health and preventing disease. But most health care organizations lack the infrastructure, consumer insights, and abilities to engage with consumers to implement this vision.

Pharmaceutical companies also have a vested interest in engaging consumers, but they are battling perceptions and negative press surrounding prices. Most people still view pharmaceutical companies as drug suppliers rather than health partners. And while these companies are good at raising brand awareness, getting consumers to inquire about a specific drug is a step away from engaging with consumers directly.

Enter the New Players

Players outside health care see an opportunity, particularly those who have (i) customer touch points or ownership, (ii) consumer engagement skills, and (iii) consumer trust. These three dimensions are all core to the DNA of large food retailers and consumer packaged goods companies. Interestingly enough, these players are being heavily disrupted in their own traditional markets by Internet-only ventures and new technologies, but they now have an opportunity to become disruptors themselves.

CPGs already occupy space in the larger nutrition ecosystem and they are hardwired to understand consumers and help them improve their consumption behaviors.

While attention is focused on how tech companies will disrupt health care, the reality is that CPGs already have the capabilities and footprint to own the consumer health care products space. They may just be sleeper disruptors—waiting until the right moment to lead the reinvention of health care.

The catch? Many CPGs broker in products that directly contribute to poor health outcomes such as fatty, high-sugar foods and drinks. To secure a strong foothold in this space, CPGs will have to prioritize healthier products, some of which will compete directly with existing lines of business. This will be challenging for some, as the quicker, easier return is in continuing to promote unhealthy decisions. But the long-term advantage of gaining consumer trust in this important market can pay dividends.

This is the strategy set by Nestlé more than 10 years ago, with a progressive shift of its investments into its nutrition and health science line of business, which has grown at a faster pace than others. Categories such as confectionery, prepared dishes, and ice creams have shrunk in size over the same period, showing a commitment to rebalance the overall company portfolio.

Retailers are also well-positioned to seize the opportunity, and some players have already made bold moves to promote health and wellness. A good illustration would be CVS’ decision to stop selling tobacco products in 2014 because it conflicted with its purpose of helping people on their path to better health. Despite discarding a $2 billion annual business, CVS has managed to grow by double digits since then, thanks to a very effective rebranding strategy and alignment of its portfolio of products and services with its new purpose.

So What Comes Next?

The consumer health care opportunity is immense with plenty of room for both CPGs and retailers to grasp key aspects of it. CPGs and retailers should focus on understanding consumer hassles and thinking beyond their normal interactions to come up with several potentially disruptive ideas.

They can then progressively shorten the list of opportunities through more thorough investigation and consumer focus groups before finally evaluating and acting on the business viability of these ideas within the framework of their overall strategy.