1.7 Billion People Don’t Have a Bank Account — But Mobile Banking Could Change Their Lives

People wear protective masks as they look at a mobile phone in Beijing, China. The average subscriptions to cellular networks are high, but the problem of low internet penetration persists and is often below global averages.

Photo: Kevin Frayer/Getty Images

Financial inclusion is imperative to achieving economic growth in a globalized market. It is also essential to achieve domestic objectives, such as poverty alleviation, anti-corruption and integrity, employment, social equity and wealth redistribution.

Globally, 1.7 billion individuals have no access to banking services, while those with access to finance pay a hefty cost for financial services.

In recent years, there has been a surge in mobile phone ownership and the use of the internet. Out of the 1.7 billion unbanked adults, 1.1 billion own a mobile phone. In developing economies, 79% of adults own a mobile phone.

Digital banking, which uses mobile and internet technology, offers an opportunity for reaching the financially excluded and underserved segments of the population, particularly in remote regions and communities. It has the potential to transform the financial inclusion landscape by offering cost-effective and easily accessible financial services.

Many Central Asia Regional Economic Cooperation (CAREC) member countries lag behind in providing services and infrastructure that are critical to increasing financial inclusion, and their digital adoption is among the lowest in the world.

A working paper examines the current state of financial inclusion in CAREC countries, excluding the People’s Republic of China (PRC). It also evaluates the potential of financial technology (fintech) for accelerating inclusion, analyzes constraints to increasing access to finance and discusses prospects of widening the net of financial services in the CAREC region.

Constraints to Financial Inclusion

In today’s world, financial inclusion goes hand-in-hand with the existence of a robust, economic and widely accessible information and communications technology (ICT) infrastructure. The quality and extent of the ICT infrastructure varies widely across the world, and this can also be seen in the CAREC region.

Economies in the region are at varying stages of development — ranging from low-income to upper-middle income with an average per capita income of $3,178. They also differ significantly in terms of socioeconomic indicators. When it comes to the provision of services and infrastructure that are critical to increasing financial inclusion, CAREC members are in general lagging in terms of access to the internet, transport linkages and government facilitation.

The average subscriptions to cellular networks are high, but the problem of low internet penetration persists and often below global averages. Without adequate internet penetration for high-bandwidth (3G, 4G, 5G) mobile technologies, harnessing fintech to achieve financial inclusion will continue to be difficult even with a high mobile subscription level.

To achieve this objective, governments need to deliver essential infrastructure, ensure a conducive regulatory environment, incentivize the private sector and build trust in financial services by protecting consumers and optimizing their experience.

Governments can lead the charge through multi-faceted measures starting with the promotion and development of quality infrastructure. It has been observed that several countries have achieved this when governments provide the initial push.

While ensuring a conducive environment for deepening financial inclusion, the governments also need to remain vigilant and act appropriately to lean against debt and financial stability risks (at the individual, enterprise and country level) that may arise as a result of unchecked, higher financial inclusion.

Key Findings

More than half of the population of the countries covered by the study are unserved by any financial service that could have potentially transformed their economic and social well-being.

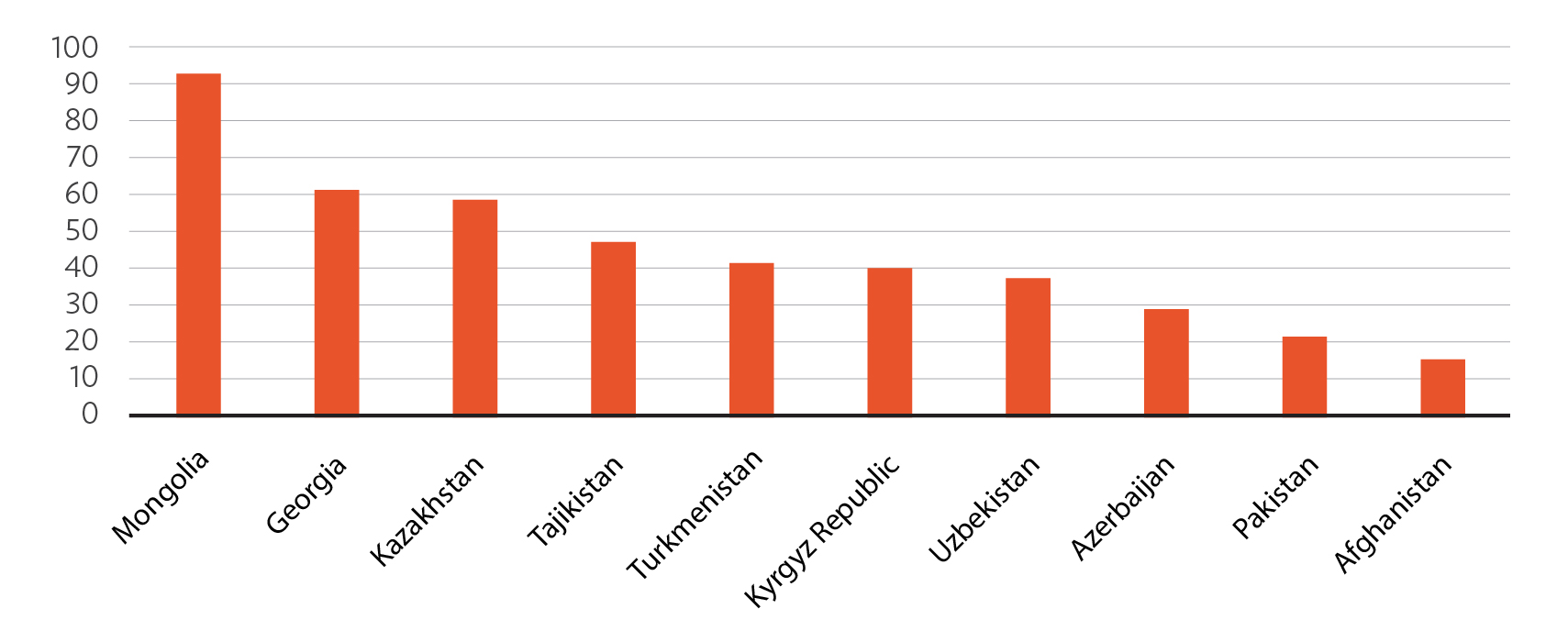

Percentage of the Population with a Bank Account

Source: Author’s calculations using data from World Bank, Global Findex Database (2017).

Mongolia takes the lead with 93% of its population owning a bank account, almost double that of the other CAREC countries. Afghanistan (15%), Pakistan (21%) and Azerbaijan (29%) have the lowest share of bank account holders in the region.

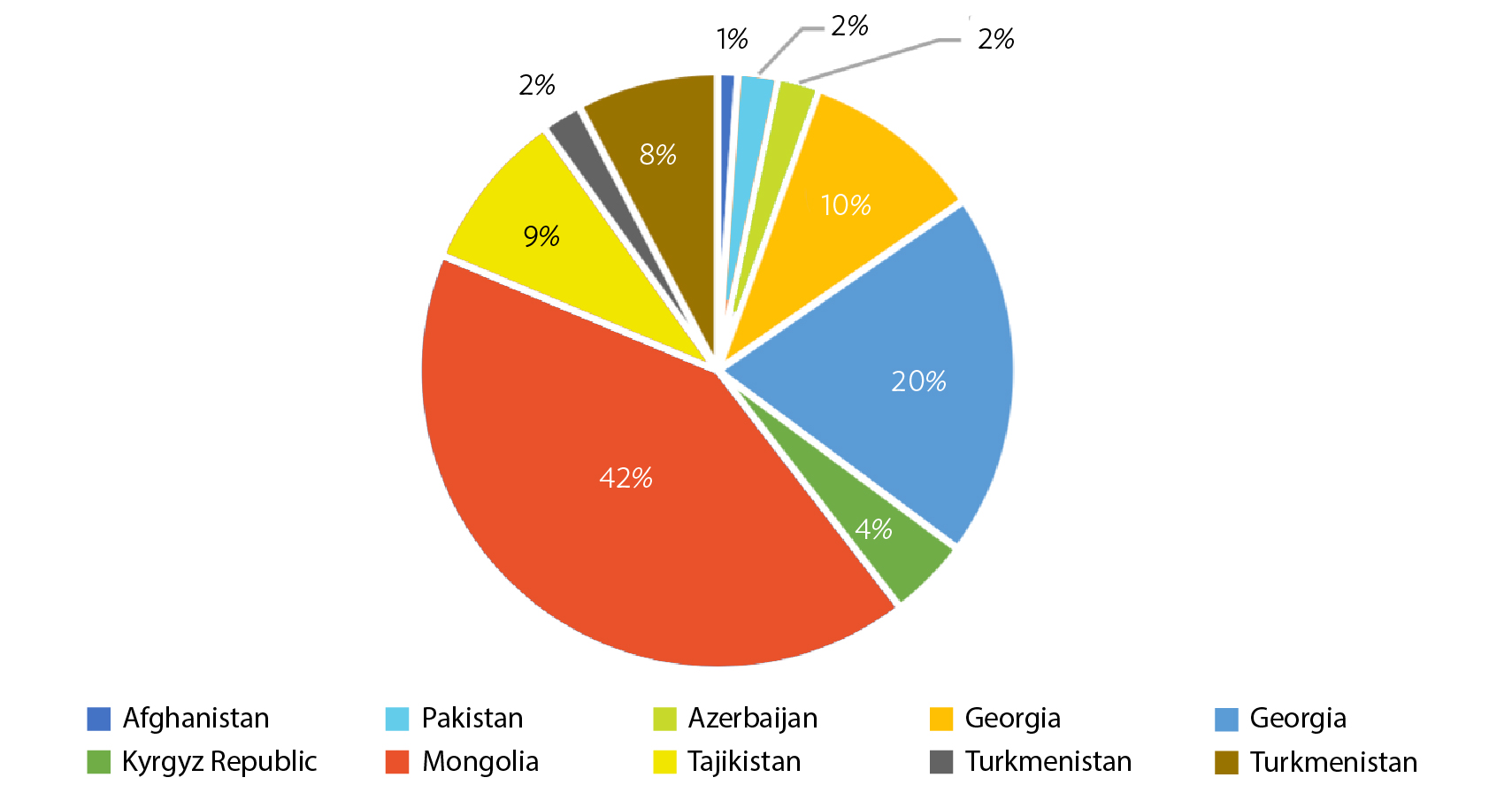

Accessing a Financial Institution Account through a Mobile Phone or the Internet (%)

Source: Author’s calculations using data of World Bank, Global Findex Database (2017). Note: Data represents individuals availing mobile phone or internet services to make or receive a payment or make a purchase in the preceding 12 months.

Two methods are typically used to access a financial account: using a mobile phone or the internet to make or receive payments digitally. In Mongolia, 42% reported using either a mobile phone or the internet to access their financial accounts in the past year. Mongolia’s high rate of using mobile phones or the internet to access a financial account is explained by its nearly universal mobile phone coverage and high level of internet penetration. Conversely, using a mobile phone or the internet to access a financial account is less common in countries like Azerbaijan, Afghanistan, Pakistan and Turkmenistan, with a share of 2%, 1%, 2% and 2%, respectively.

Going Forward

CAREC countries can learn from regional and global success stories, which can help finetune and tailor their policies according to the local context. The People’s Republic of China and Kenya present distinctive success models to emulate. The PRC, with its peculiar economic and political system, thrived on the back of a formal banking sector account ownership, primarily supported by the state-owned banks and creatively led by tech giants. On the other hand, Kenya, a relatively smaller economy, relies on its private sector to take and absorb risks and lead the drive to financial inclusion, while the government provides ideal conditions for innovation to thrive.

To increase financial inclusion using fintech, governments and multilateral development partners need to collaborate to develop synergies and find affordable and sustainable solutions to improving financial inclusion.

Governments need to take the lead by providing an enabling policy environment that should be embedded in an integrated national financial inclusion strategy with defined and measurable targets supplemented with a robust implementation mechanism.

Governments must design and adopt a digitalization policy to shape the direction of digital adoption in the country. Governments must make concerted efforts to develop and promote an enabling ecosystem to support innovation. The outbreak of the COVID-19 pandemic has further amplified the need for a digital revolution.

Developing and enacting a supportive legal and regulatory system is one of the essentials of propelling financial inclusion. The regulatory environment needs to accommodate disruptive innovation led by startups as well as incumbent big players in finance and technology. Consistent with national financial inclusion strategies and digital adoption policies, the countries need to upgrade their legal frameworks, which are skewed in favor of “business-as-usual” financial services. However, caution needs to be exercised as there are no one-size-fits-all solutions available. Governments need to carefully formulate legal and regulatory policies conducive to a country’s economic context.

Elevating levels of trust in the banking and financial sector and bridging the access gap necessitates multi-faceted policy measures. Governments should not just leave it to the private sector to design financial inclusion products and deliver to underserved adults. They should reinforce people’s trust in financial products offered by the private sector. Targeted efforts on the part of the governments would help ensure equitable provision of financial services across gender, income groups and age groups.

CAREC countries need to engage the private sector right from the beginning — from conceptualizing the financial inclusion strategy and drafting digital adoption policies to developing a legal and regulatory framework. The critical role of the private sector in innovation and service delivery cannot be overemphasized. In many countries, the private sector has led the growth of account ownership and adoption of fintech.

In addition to technical support, development partners’ financial assistance is critical in developing vital financial and technological infrastructure. They can extend loans, technical assistance, equity investment and grants to governments and the private sector to help raise the financial inclusion level.

This piece was originally published in Development Asia.