Cargo ships travel on Yangzte River waterway in Maanshan, central China's Anhui province. The most tangible economic evidence of the decline of globalization is that global trade is no longer driving global growth to the extent it has historically.

Photo: STR/AFP/Getty Images

Two defining characteristics of globalization—increased global trade and greater economic participation in trade—now look poised for an extended downward trend.

If we add to this economic circumstance a global political overlay that is polarizing to the tails of the liberal-democratic distribution, then we could expect a sudden stop, and perhaps a significant reversal, in globalization. Dynamics such as “localization” will rise in place of globalization, driven by protectionist policies and those who seek to woo polarized voters by promising an onshoring or reshoring of jobs that are popularly perceived to have been lost or stolen.

The decline in world merchandise goods trade as a percent of GDP, cross border lending and foreign direct investment (FDI), and the increase in protectionist measures together will have profound implications for cross border global flows. Any reversal of these multi-decade dynamics is likely to be most apparent in Asia—and the Mekong Subregion in particular.

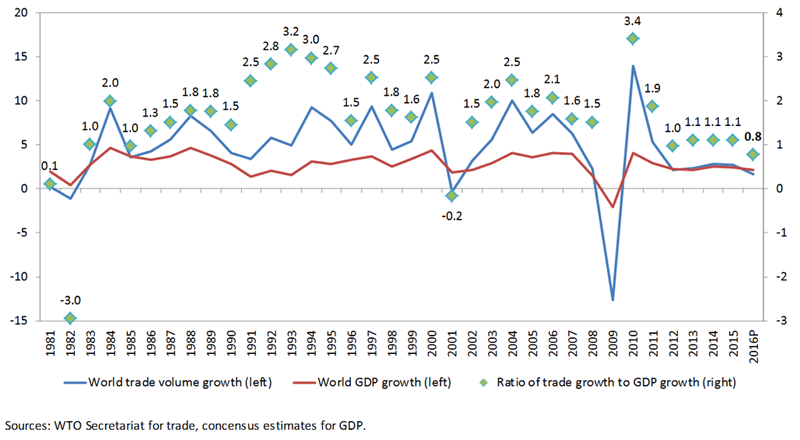

The most tangible economic evidence of the decline of globalization is that global trade is no longer driving global growth to the extent it has historically. 2016—and possibly 2017—are expected to join that small set of aberrant years where the ratio between trade growth and world GDP growth is less than 1:1 according to latest forecasts from the World Trade Organization.

The relationship between world merchandise trade and GDP growth has broken down.

Have We Reached the Globalization Endpoint?

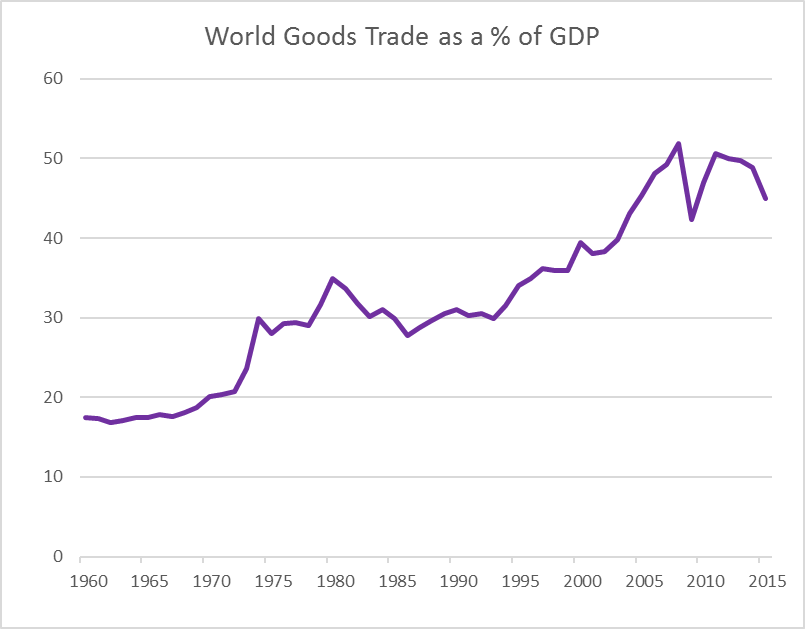

Greater economic participation in trade is clearly in a downturn. World merchandise goods trade as a percent of GDP appears to have peaked in 2008 (after briefly declining from 1980-1986 owing to the 1980s oil glut that followed peak oil prices in 1980).

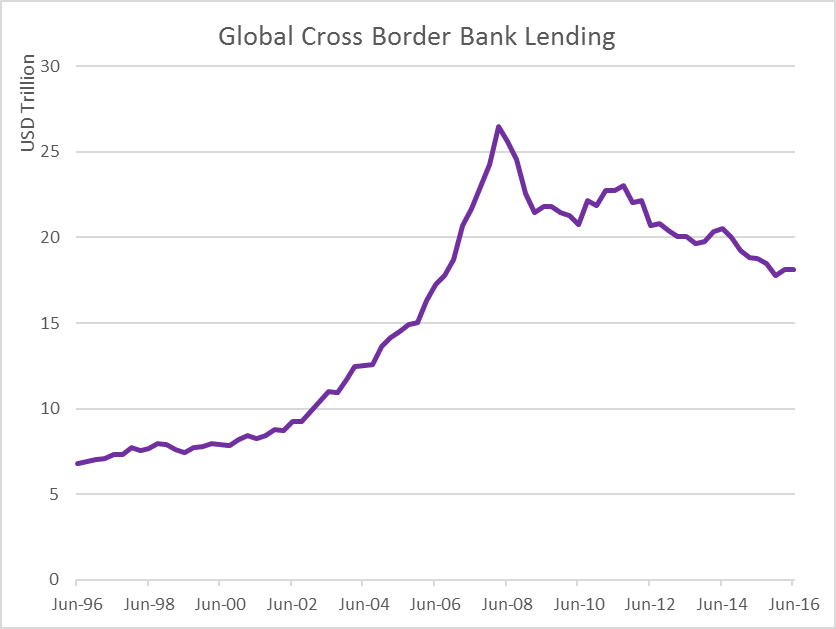

Further, a key enabler of globalization—the free flow of financial capital across borders to finance the building of production facilities or mergers and acquisition activity—also appears to have mirrored this pattern, peaking alongside trade.

World goods trade and cross border lending are slowing. Source: CEIC and World Bank

Source: CEIC and Bank for International Settlements

This pull back in cross-border bank lending would not be as problematic from a globalization perspective if cash-rich, non-financial corporates bore more responsibility. However, the top 5,000 multinational enterprises have been pulling back on direct capital investment and overseas acquisitions in an environment of political uncertainty and dramatically rising protectionist barriers to trade in recent years.

According to their latest forecasts, UNCTAD expects the world’s largest companies to invest 10 to 15 percent less in their overseas operations in 2016, effectively trimming FDI by around $250 billion.

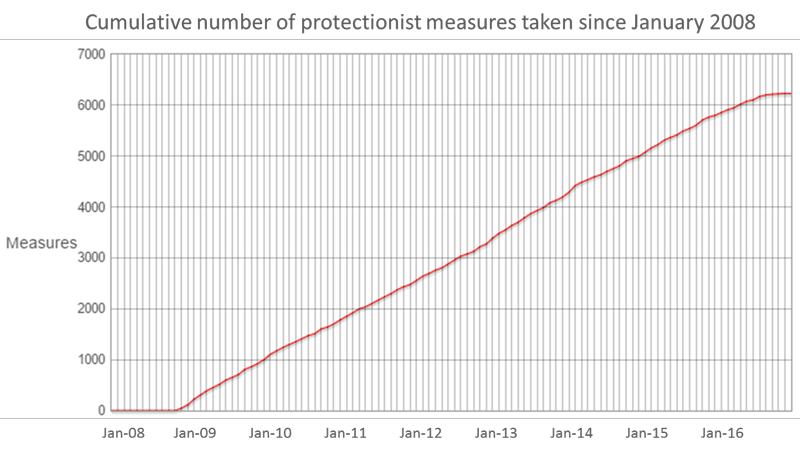

Finally, the political pushback against the free flow of people across borders has become one of the key issues of 2016. The effects of this push back can also be seen in the dramatic rise in temporary protectionist measures since January 2008, as measured by the independent Global Trade Alert. The protectionist measures have risen from virtually zero to over 6,300 separate short-term trade restricting measures as of October 2016.

Protectionism has risen dramatically. Source: Global Trade Alert

The current period seems to be the only one in modern economic history where all three key metrics of globalization—the cross border flow of finance, people and physical capital—are declining.

Tensions at the Intersection of Economics and Politics

Tensions are most readily apparent where the economics and politics of globalization meet. The Brexit vote and the subsequent rise of nationalism in the EU and the vitriolic 2016 U.S. election campaign have been the headline grabbers to date.

Even China—often painted the culprit for developing economy woes—has not been immune to populist sentiment that has shaped anti-globalization forces elsewhere in the world.

It is not surprising that China’s recent policies and focus have also included a dynamic of “localization” to ensure employment stability. This has had an indirect but immediate effect to the ASEAN and the Mekong Subregion as China has essentially shortened value chains used in its own production and is now vertically-integrating or domiciling labor-intensive components of production onshore rather than offshore.

When China started rebalancing its economy away from investment and exports to a more consumption- and services-led growth model in 2011-12, many hoped that this would usher in a wave of globalization, more fully embedding the ASEAN economies of Thailand and Vietnam in global value chains, and for the first time extending those value chains to the Mekong frontier economies of Cambodia, Laos and Myanmar.

That outcome now seems less certain and the consequences of this are potentially profound.

How Will the Asian Growth Story Unfold?

Every Asian economy that has successfully industrialized and modernized has used labor-intensive manufacturing, such as in clothing and apparel, as its nursery or incubator to build a manufacturing workforce. As production-line skills were learned, and technology and skills transfer enabled a deepening of the skill set of the local population, particularly when coupled with vocational training, low-income economies have been able to ascend value chains into middle-income economies and eventually succeeding in traversing the middle income trap.

The globalization end-point, if we are indeed at it, would suggest that using industrialization and trade as a mechanism for economic convergence stops with China (or indeed China’s coastal provinces). Those economies that have only taken the first tentative steps to industrialization and convergence could find their progress disrupted, perhaps even halted.

The result could be a more dichotomous Asia, characterized by those economies that have used trade and industrialization to traverse the middle income trap, and another group of economies who will have to engineer different and more imaginative convergence mechanisms if they are to do the same.