With the high level of uncertainty and economic recovery taking many different shapes, understanding the outlook for the housing market resembles a jigsaw puzzle.

Leading up to the pandemic, the United States housing market was showing incredible resilience, and even promised to be the strongest year since the Great Recession. With some lulls along the way, particularly in late 2018, home sales at the beginning of 2020 reached the highest level since 2008.

The strength of the housing market coming into 2020 was in part due to very low mortgage rates along with scarcity of homes for sale (mostly among affordably priced homes) and strong employment and income growth.

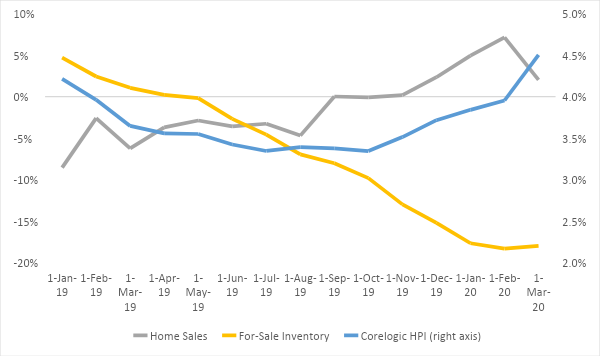

As Figure 1 suggests, a pickup in demand also reinvigorated home price growth, which reached 4.5% year-over-year increase through March, according to the latest CoreLogic Home Price Insights (HPI®) Report.

Figure 1: Year-Over-Year Percent Change in Monthly Home Sales, Inventory and HPI

Source: CoreLogic Home Price Insights (HPI®) Report

A Pandemic Changes Everything

And then, COVID-19 happened. In the wake of President Donald Trump’s declaration of a national emergency on March 13 and a number of shelter-in-place orders across the country, most housing market indicators took a turn almost immediately.

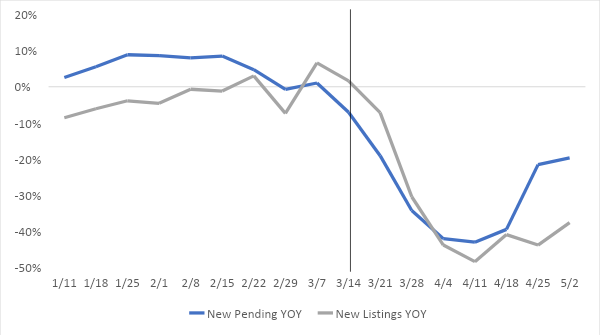

Pending sales, which are considered a leading indicator for sales expected to close in 30 to 45 days, quickly started declining; they fell 40% by mid-April, compared to last year’s levels. New for-sale listings followed a similar trend, also falling by half compared to last year.

Figure 2 illustrates pending sales and new listing trends on a weekly basis since the beginning of 2020. After reaching a trough by mid-April, the two indicators have shown some signs of a turnaround, suggesting that home buyer activity is slowly rebounding. Nevertheless, with such a remarkable pause in home-buying activity throughout April, forthcoming home sales data for April and May will likely show significant declines compared to previous years’ spring buying seasons.

Figure 2: Year-Over-Year Percent Change in Weekly Data for Pending Sales and New Listings

Source: CoreLogic Home Price Insights (HPI®) Report

Home Prices Still Stable

While home-buying activity has been severely affected by the pandemic, home price growth has remained relatively steady. That is in large part supported by housing market fundamentals leading up to the pandemic, such as lack of availability of homes for sale and eager first-time home buyers looking to take advantage of historically favorable mortgage interest rates.

Home price growth in April and May is still expected to show a 12-month increase of more than 4%, while the national forecast through March 2021 suggests deceleration of price growth to 0.5%, but no significant decline.

Now, with the high level of uncertainty and economic recovery taking many different shapes, understanding the outlook for the housing market resembles a jigsaw puzzle. Home-buying activity is showing signs of a pickup from a trough as more sellers are willing to put their homes on the market and as more home buyers apply for mortgages and enter into contracts.

All Depends on Millennials

The rebound in mortgage purchase applications is still mostly driven by millennials in their search for a first home. According to CoreLogic data, millennials’ April mortgage applications were down only 7% compared to last year, while applications among the other generations declined between 30 to 40%.

With the extent of the job losses and potential impacts on household budgets, it is unclear how many prospective buyers, including millennials, will be held back in the future. Overall, housing market observers are widely expecting 2020 home purchases of existing homes to contract by about 15% compared to 2019, and rebound at a similar rate in 2021.

Nevertheless, housing market outcomes will vary considerably across the metropolitan areas, as the pandemic has had a varying impact on local economies and the severity of the health crisis has differed. CoreLogic mortgage applications again suggest that some regions, such as Dallas and Houston, have seen a smaller decline in mortgage application activity than COVID-19 epicenters such as New York, Los Angeles and Philadelphia.

Local Economies Will Vary

Going forward, diversification of the local economies will play a critical role in a region’s ability to bounce back. As we already know, industries that have suffered the largest losses due to the pandemic — such as the leisure and entertainment, retail, education and personal services, among others — may have to permanently change their operations.

This will have a significant impact on some local economies, as well as people employed in those sectors. An open question is how that will change the urban structure and desirability of certain metropolitan areas. Many are speculating that households will seek to move to areas with more open space and away from high-density central business districts and high-rise residential.

Also, the adaptation to remote working, accelerated by the pandemic, may lead to demand for larger homes that include a separate office and are not dependent on transit or employment accessibility. That’s a major shift in preferences for many families from pre-pandemic times.

Will Second-Tier Cities Fare Better?

There are also questions on the reuse of retail spaces and potentially office spaces as e-commerce and remote working take on a life of their own.

The truth is that it is still very early to tell, though some changes to consumption preferences will definitely take place. If the latest data suggests future trends, second-tier cities’ affordability and lack of density may promise a relatively stronger housing market compared to the urban core of large metropolitan areas; however, the size of large metropolitan areas may sometimes mask the changes that are happening within those microcosms.

For rental homes, we may see tenants more likely to renew leases and stay put for the next several weeks. Once the U.S. has made it through the pandemic, we may see renters more often opt for larger rental spaces and single-family homes over multifamily apartments.

For some tenants, this could meet a desire for a home-based office and for greater distance between housing units. All of these changes in preferences will have an impact on spatial organization of our urban areas. And lastly, the acceleration in innovation brought about by the pandemic is sure to guarantee greater productivity in many sectors and open doors to possibilities we haven’t thought of yet.