Commodity Futures Trading Commission Chairman Rostin Behnam prepares to testify about the collapse of the cryptocurrency exchange company FTX on Capitol Hill on December 1, 2022.

Photo: Chip Somodevilla/Getty Images

On Friday, November 11th, cryptocurrency exchange FTX Trading Limited (“FTX”) and its sister cryptocurrency trading firm Alameda Research (“Alameda”) filed for Chapter 11 bankruptcy. Just a week earlier, on Monday, November 7th, Sam Bankman-Fried, founder of both companies, had tweeted, “FTX is fine. Assets are fine.”

How exactly FTX and its sister company crashed is still being uncovered. FTX had been valued at $32 billion just a few months ago. There is alleged fraud. Many retail and institutional investors may not recoup their assets currently frozen on FTX. Some — including Sequoia Capital, BlackRock, and Ontario Teachers’ Pension Plan — had invested in FTX. Meanwhile, FTX and Alameda Research had invested in more than 250 startups building out decentralized finance (DeFi), cryptocurrency, and blockchain ecosystems.

Many are understandably shocked, dismayed, infuriated, and feel Sam Bankman-Fried deceived them.

However, some reactions reflect misconceptions about fundamental concepts, including decentralization, cryptocurrencies and blockchains.

These umbrella terms house many different kinds of technologies, people and processes that investors must navigate in order to appropriately assess potential risks and rewards.

1. ‘This Shows Why We Need Decentralized Finance’

Some are rejecting centralized finance writ large by its association with FTX, a centralized cryptocurrency exchange that requires users to trust their money with a third-party (Sam Bankman-Fried and team). Many are instead turning to DeFi in response.

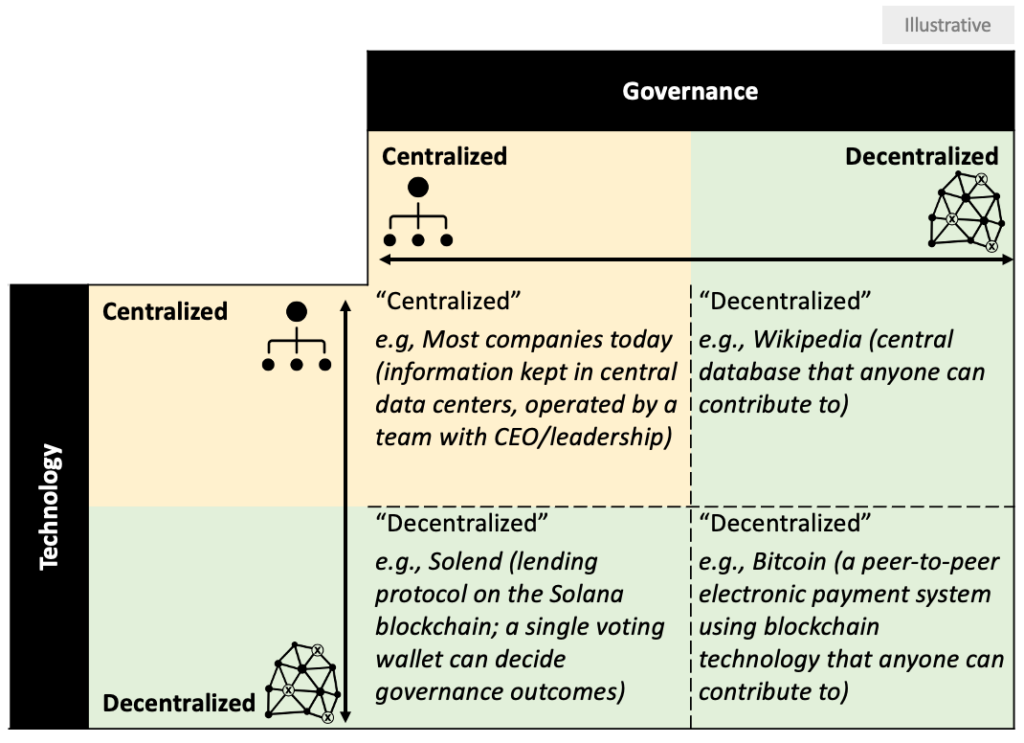

DeFi comes in many forms. Some forms require trusting third-party actors. The term “decentralization” can refer to 1) technology and/or 2) governance. This is a critical distinction. Investors who mistakenly conflate decentralized technology with decentralized governance may unwittingly be trusting third-party actors.

Figure 1: Nominally “Centralized” and “Decentralized” Technology vs. Governance

Additionally, decentralization and centralization are not black-and-white concepts; they represent the ends of a wide spectrum. For example, blockchain is generally regarded as a decentralized technology, but there are ongoing debates about the extent to which certain blockchains are decentralized in governance (see section 3 on blockchain technology below).

There are two primary questions to ask when assessing to what degree an entity/exchange/project (“entity” hereafter) is decentralized or centralized:

- What technology do they use, and to what degree is the technology decentralized?

- Who makes decisions about the future of the entity, and to what degree is the decision-making process decentralized?

There are many cases where DeFi entities use decentralized technology but have arguably centralized leadership teams. Serum, a “decentralized” cryptocurrency exchange on the Solana blockchain, describes itself as a decentralized autonomous organization (DAO). DAOs are member-owned organizations with built-in rules enforced by code stored on blockchains. The built-in voting rules can lend to a high degree of centralized decision-making. Serum’s built-in voting rules enabled a single wallet — allegedly controlled by Alameda — to pass proposals.

Centralization does not necessarily lead to bad outcomes, and decentralization does not necessarily lead to good outcomes — and vice versa. Investors turning to DeFi in reaction to the downfall of FTX must specify which components of DeFi they want to embrace.

2. ‘Crypto Is Dead’ Vs. ‘Crypto Is the Future’

Some argue that “Crypto is dead,” whereas others argue that “Crypto is the future.”

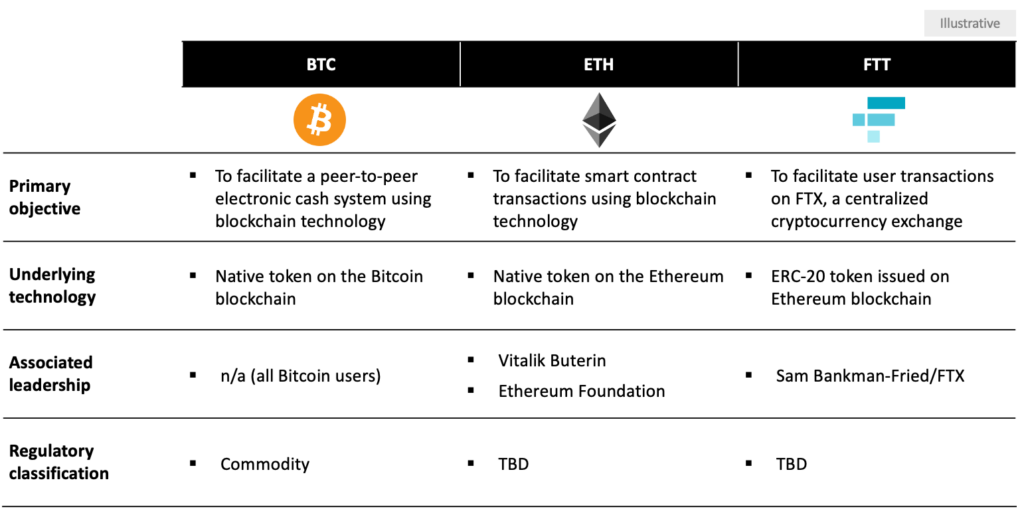

Not all “crypto” is equal. For example, BTC, ETH, and FTT do not share the same underlying objectives, technologies or governance structures. They may diverge even further when regulatory classifications emerge.

Figure 2: Comparison of Different Cryptocurrencies: BTC, ETH, FTT

In the aftermath of FTX, many cryptocurrency investors are concerned about how third-party activity may impact the price of cryptocurrency assets.

A key question to ask when investing in cryptocurrencies: Is there a central entity commonly perceived as the “leader” in association with the cryptocurrency?

Centralized leadership can inordinately influence an asset’s price. FTX, for instance, would regularly repurchase and destroy some of its FTT tokens in circulation, directly driving up the price. The fall of FTX has directly sent the price of FTT tumbling.

The current lack of regulatory clarity makes it challenging to use more precise terminology to help distinguish different kinds of cryptocurrencies. For instance, it remains unclear whether some cryptocurrencies, including Ether, will be classified as a security or a commodity.

The value of any cryptocurrency — and fiat currency — is ultimately a social construct. If enough people believe a currency is valuable, that currency becomes valuable. For cryptocurrencies, their primary objectives, underlying technology, associated leadership and regulatory classification will likely shape their respectively perceived values. A cryptocurrency whose primary objective is to facilitate profitability for a centralized exchange whose leadership is dishonest and disorganized is unlikely to be perceived as valuable over time.

Time will tell which cryptocurrencies will continue to be valued long-term.

3. ‘Trust Only the Immutable Blockchain, Instead of Humans’

Blockchains — as with any technology — are only as trustworthy as the people who build and operate them (see here for a primer on blockchains, which are digital record-keeping systems). Blockchains also come in many different forms.

There are two primary questions to ask when navigating different blockchains:

- What kind of blockchain is it — private or public?

- What is the underlying consensus mechanism?

First, while all blockchains use decentralized networking technology, not all blockchains are decentralized in governance. A key distinction lies in private versus public blockchains:

- Private blockchains typically have more centralized governance than public blockchains and require placing trust in a third-party authority that owns the network. Private blockchain networks are sometimes referred to as “permissioned” because individuals require authorization from a centralized body to participate and transact.

- Public blockchains allow anyone with access to the internet to transact while maintaining anonymity and are sometimes referred to as “permissionless.” Public blockchains tend to have more decentralized governance than private blockchains. However, public blockchains differ significantly in the degree to which they employ decentralized governance. Consensus mechanisms are key differentiators. “Consensus mechanism” refers to the decision-making process governing what information gets officially recorded on a blockchain. Today there is heated debate about whether proof-of-work or proof-of-stake, the two predominant consensus mechanisms used in public blockchains, can provide more decentralized governance.

Second, blockchains are not actually immutable. “Immutable” suggests that records on blockchains cannot be changed or deleted without exception. All blockchain ledgers can technically be changed. The same consensus mechanism used to create blocks can be used to modify/undo. Typically, adding new blocks is intentionally made difficult for security reasons; the more difficult it is to do, the more difficult it is to undo. For example, to change official records on the Bitcoin network, one would need to amass 51% of the computing power on the network. To change official records on the Ethereum network, one would need to amass 51% of ether staked by validators. Numerous instances of 51% attacks have successfully reorganized transaction history, leading to stolen funds.

Decentralization, Cryptocurrencies, and Blockchains Come in Diverse Forms

Since the downfall of centralized exchange FTX, its token FTT, and its former CEO Sam Bankman-Fried, some investors are seemingly putting trust in nominal opposites — DeFi and blockchain technologies. Some have been quick to dismiss all cryptocurrencies. Yet, DeFi, cryptocurrencies, and blockchains come in many shapes and forms.

In traditional finance, subprime mortgages have very different risk profiles from prime mortgages — despite belonging to the same umbrella term, “mortgages.” Similarly, not all entities that claim decentralization are the same, not all cryptocurrencies are the same, and not all blockchain technologies are the same. Understanding the different and diverse components of each umbrella term is crucial to assess potential investment risks and opportunities appropriately.

This article originally appeared on https://metaverselife.substack.com/